If you choose not to decide, you still have made a choice.

- The late Neil Peart

Failing slow

- Cash is safe in the short term, but remember it has lost >95% of its value in the past 100 years due to inflation. Wealth held in cash slowly erodes.

Failing Fast

- If you lose 33% of your wealth, you need to return 50% to get back to even. If you lose L you need to make L / (1-L). That formula reminds you that taking too much risk for your needs is how you fail fast.

Investing is not a choice. You can fail fast or fail slow.

The Retirement Problem

You work for 40-50 years but you live for 20 to 30 years more. The problem you must solve: don’t run out of money.

The only certainty is if you save (ie spend less than you earn) this will lower bar for retirement income and lower the need to reach for investment goals. Before worrying about investing be wary of "lifestyle creep". You adapt to nice things. It's called hedonic adaptation which is a fancy way of saying your happiness mean reverts.

Sequence of Return Risk

From Movement Capital:

Returns in early retirement can mean the difference between leaving a substantial legacy or running out of money. That’s called sequence risk, and sequence risk is amplified as portfolio withdrawals increase.

Three ways to reduce sequence risk include

- Dynamic portfolio withdrawals

- Cash buffers

- Investment strategies that reduce drawdowns.

The exercise you should do

Try the Moontower Retirement Model to simulate your own finances to get a feel for the money levers in your life.

You can access the Google sheet here: Moontower Model

- Go to file: Make A Copy

- See this post for discussion

https://moontowermeta.com/the-moontower-retirement-model/

The Retirement Problem

You work for 40-50 years but you live for 20 to 30 years more. The problem you must solve: don’t run out of money. Retirement finance is a vast field filled with overly precise mathematical treatments of “safe withdrawal rates” and investment allocation “glide paths” (think a target-date fund that is aggressive when you are young and conservative as you age). William Sharpe who won the Nobel Prize for the CAPM model called it the hardest problem in finance.

I’m not going to bore you with all that. I’m also not going to bore you with my soapbox rant about how destructive I think the whole vision of retirement is as portrayed by Charles Schwab commercials. The fact that it takes a moment to figure out if it’s a financial commercial or a Viagra ad is enough of hint that drugs are being sold in both cases.

Instead, I will encourage you to walk through an exercise that identifies the most important levers of the problem. I’ve put together a Moontower Retirement Model that you can make a copy of and play with your own numbers. I built it years ago and because of back and forth in my Whatsapp chat had a chance to dust it off and improve it. The model’s value is not in its output. “Hardest problem in finance”, remember?. It’s laden with assumptions and simplifications. It also spits out a path without confidence intervals. You can’t get away from the shortcomings. But if you have never worked through something like this, you are going to think about money in a much more enlightened way afterward.

Here’s the Moontower Retirement Model

(Please don’t hesitate to ask questions, point out errors and so forth. I’d like to enhance it over time.)

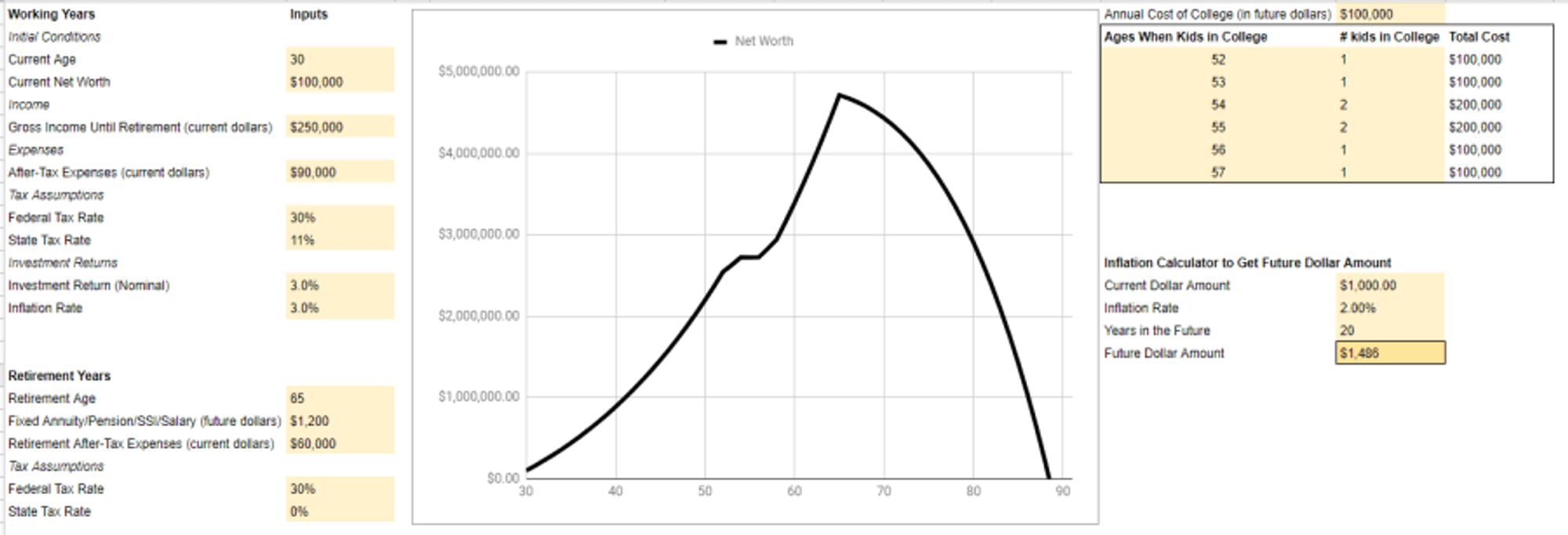

Here’s a screenshot of the input screen:

You will have fun trying to estimate numbers for your household income and expenses and if not it may alert you to get a grasp on these things.

Once you have some reasonable assumptions start tinkering with:1) Inflation and investment return rates

Inflation is applied to pay and expenses evenly. Investment returns are applied to your entire net worth. Since net worth includes cash, homes, and stocks try to estimate a decent weighted-average return.

2) Retirement Age

Every year you delay retirement has a double impact. You increase savings that can grow AND you don’t withdraw return-generating assets.

3) Savings

A dollar saved is another source of big swings. You not only reduce the expense but you reduce the compounding of that expense. Or you can say that a dollar saved is also extra dollars in the future due to compounding. This is the most interesting lever because it’s high impact and insofar as you can control your expenses, it’s the lever you can steer the best. In contrast to, say, inflation. Good luck understanding inflation nevermind controlling it.

Don’t focus on the specific numbers as if you saw your future. You didn’t. This exercise has immense value despite that.

Learn More

- Nick Maggiulli's Twitter thread: Uncomfortable Truths About Investing (Link)